“No go, unfortunately.”

That was the text from a contact saying her spouse wouldn’t be able to talk to us for this piece. As a critical care physician who’s spent the last year and a half treating COVID-19 patients and is now taking an extended sabbatical to recover, he was the perfect source for an article looking at the current state of the healthcare workforce – the accelerated burnout, the frustration, the fear and the sheer exhaustion. We had questions lined up: What do doctors and nurses need today? How much does monetary compensation play into the equation versus other types of support? Do the rumblings about an exodus from healthcare represent a real threat? Where do you hope to be after your time away?

But no, we would not be asking those questions. And maybe, that makes the story more powerful. Because the reason that this elite physician couldn’t talk to us wasn’t a matter of practicalities and scheduling. It was because he has given everything to save as many people from COVID-19 as possible and has nothing left. “He just shuts down when we talk about COVID,” the spouse said.

That absolute exhaustion encapsulates the problem our entire healthcare system is facing today. It clarifies both the human cost and the operational challenges facing provider organizations.

This report, based on interviews throughout the Jarrard Inc. network of clients and experts, triangulates the trends, draws conclusions about the future and offers thinking on how to manage an issue that’s gone past the boiling point.

That’s the public side, though. How much do the headlines reflect what’s happening behind closed doors? And, how much of an impact are we seeing from the visible PR battle combined with the results of closed-door negotiations? What’s the public perception of providers and payers? Does it even matter?

To determine whether payer-provider relationships are under more strain than usual, we spoke to experts in our network, checked in with our team and polled the public.

What we summarized: The cold war is heating up. There’s pressure on and from both sides, and a growing feeling of “Us” vs “Them.” Publicly, the balance of the PR is weighted towards payers, thanks to the campaigns mentioned above. But the insurance industry has a way to go to convince the public of its good intentions.

What We’re Hearing

Overall, payers and providers are getting more aggressive. Historically, negotiations tend to follow a set arc, with long, tense conversations bumping up against the expiration date only for a deal to be struck at the eleventh-and-a-half hour. While that remains largely true, the tone of more negotiations is getting hotter, the demands bigger. And in some cases, according to sources, the conversations nastier and more personal – with some individuals pointing fingers at the people across the table, not the organizations represented. That’s a problem.

As both providers and payers get bigger, it makes sense that the stakes would get higher. Each side is looking for leverage, and size is leverage. There are many reasons why hospitals pursue mergers and partnerships. Strength to push back against payers is certainly one of them.

An Elephant in the Room

Or, ahem, at the negotiating table.

Last year, as the CMS price transparency rule loomed, a big question was how the posted data would be used. Providers were concerned the data would be of marginal value to consumers – but a gold mine to competitors and other industry stakeholders. Eight months on, that’s looking more likely.

Sources tell us those numbers are beginning to come into the national discussions around price. While the data are far from perfect – in some cases they’re not even that great – they could begin to affect payer-provider negotiations.

M&A skeptics (including the White House) like to note that “The top 10 health systems now control 24 percent market share,” according to Deloitte. Yes, and, the five biggest health insurance companies control 44 percent of the market. Half as many players controlling almost twice as much relative territory. So, joining forces with a larger system that can help balance the weight makes a lot of sense for a smaller provider.

Still, it’s not all brass knuckles. “I’m seeing more candid discussions and true attempts to find middle ground,” said James Kennedy, a Tampa-based shareholder and chair of the healthcare practice at Carlton Fields. Greg Maddrey, director at Chartis and president of Chartis Consulting, said he’s seeing a mix of discussions:

“We see very collaborative discussions in some parts of the country and contentious discussions in other regions. It depends on the payer and market. One system just negotiated a significant value-based program, and they are exploring additional opportunities for JVs/collaborations. In other areas, the negotiations seem like traditional zero-sum game models.”

Things Usually Work Out, But…

We’ve also seen recent examples of things falling apart, eleventh hour or not. As the players get bigger, so do the numbers of patients who will suddenly find themselves walking into an out-of-network facility. Then comes the finger pointing as both sides try to pin the blame on the other. “They’re too expensive!” says the payer. “They’re raking in profits and want us to take less!” says the provider. “We’re trying to find a solution for our patients,” both exclaim. Meanwhile, patients are left scrambling, confused and footing the out-of-network bill.

Fortunately* for providers, the public is on their side. Or at least, more on their side than on the side of payers. We recently fielded a survey of American adults to get past the noisy headlines and figure out what the public actually thinks.

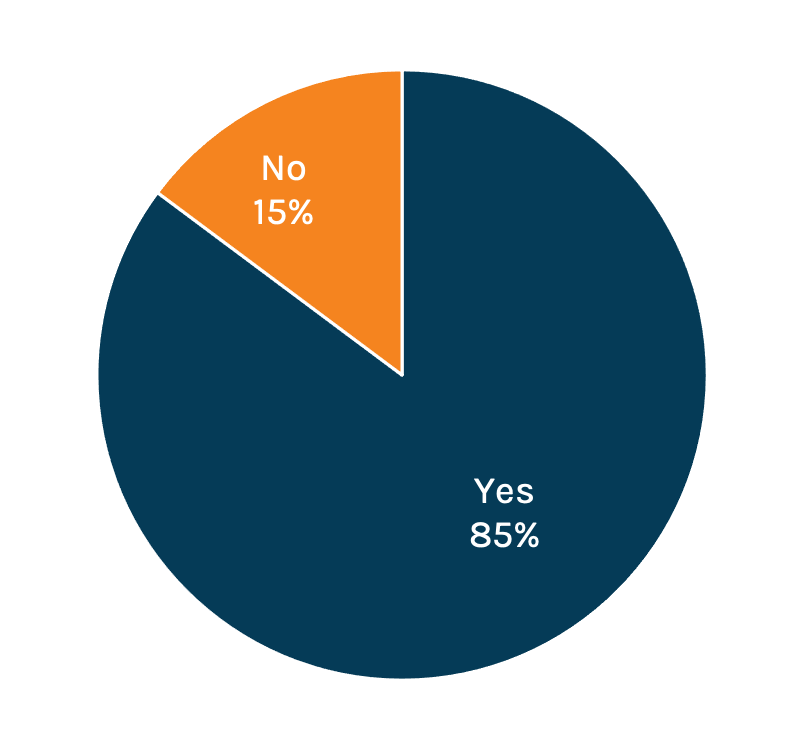

Do You Think Healthcare in the US Costs too Much?

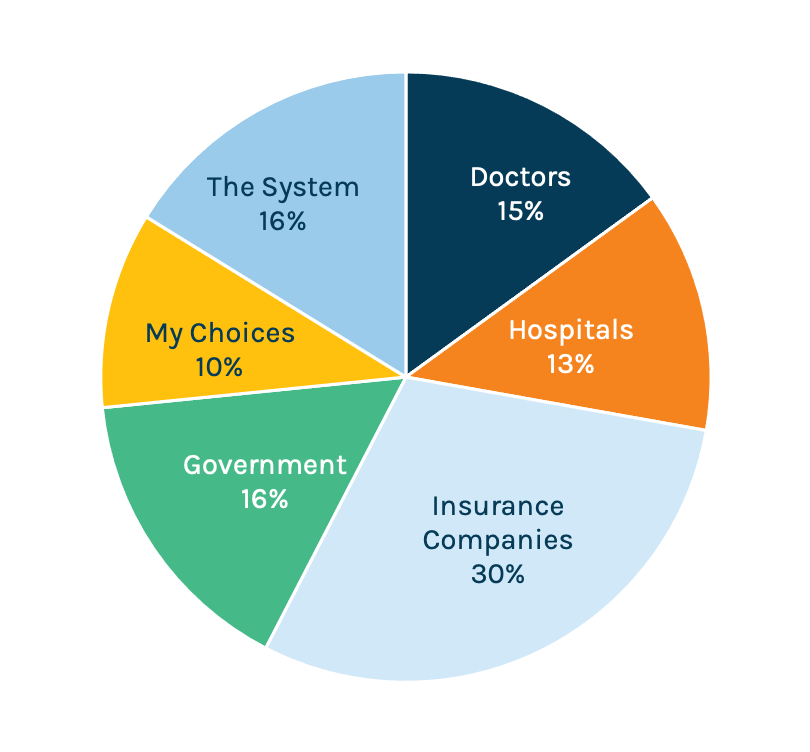

Who is Primarily Responsible for the Cost of Care?

Most everyone (85 percent) agrees that healthcare is too expensive, and 30 percent of consumers believe the insurance industry is to blame. Only 13 percent blame hospitals for the high cost of care. Makes sense, then, that insurance would want to reposition itself in softer, friendlier light. It also follows that health insurance advocates would want to shift some of the blame to hospitals.

*About that asterisk: Hospitals should be pleased that they retain more of the public trust than other healthcare stakeholders. But they shouldn’t take that trust for granted. While the headline-grabbing ongoing campaign against hospitals doesn’t seem to have taken hold in the public’s mind yet, nothing says that it won’t.

What Happens Next

On paper it looks like providers are facing a multi-front battle, with skirmishes breaking out in places and tensions rising in others. How do you, as a provider, prepare for the impending charge? By going on the offensive.

Publicly

Explain your value. Repeatedly. Specificity is the antidote to speculation. Be aggressive in presenting data that shows how your organization contributes to the community it serves. Patient visits, lives saved, babies delivered, cancers caught early, people employed, economic impact. If your hospital reflects the local demographics, if you have a career development program to help improve diversity at the upper ranks, if you have a unique recruiting program to bring in more diverse physicians – talk about it. (If you don’t, start working in that direction). Talk about what you do with the revenue that comes in. Explain where that four percent margin you make is reinvested.

But don’t get mired in the data. Personalize it. Use stories to illustrate the numbers. Need a sign that stories are effective? Look no further than the “other side” of this debate. Hospital critics have been far more effective using stories to illustrate purported patient harm. They’re masters at personalizing the numbers they’re attacking. The public can see and hear patients and the pain they’re suffering. In contrast, providers, so far, tend to speak in numbers and vague platitudes. It’s no contest.

Explain how healthcare finance works. Did you cringe? Fair. Explaining the complexities of healthcare is brutal and daunting. But it’s on you to simplify the complex (or call in the experts to help you with that). Clear is kind, right? The more absurdly dense something is, the harder you need to work to explain it clearly, and dispel any sense of covering up, hiding facts and being opaque. Your patients and the public will appreciate you for that.

More Smart Strategies

Keep these tips in mind to navigate public disputes with payers

Advance preparation is key

Strike first to frame the issue

Clear, patient-centric messaging is most powerful

The messenger matters most: Clinical spokesperson is key

Establish a single source of truth online early on

Tactics & tone must match culture

Marcom obviously plays a lead role here. It’s time to develop educational materials to explain how insurance and billing works, and what patients’ options are. Not the inscrutable, low-quality papers that look like they came off a 90s copier, but attractive resources that explain in simple language what the terminology means, where people should look for information and how to interpret what they find. Video is helpful, or even social media posts to talk through the basics. Finally, work with your rev cycle team to ensure that anyone who might interact with patients on billing is trained to answer questions…in a friendly way.

One more thing here. While you’re translating the basics healthcare finance to your patients, think about going public. Seek out opportunities to talk in public forums. Use the media. Be a resource for reporters who are covering these issues. Don’t wait until they call you with tough questions. Position yourself proactively as the one offering information.

Privately

Get networking – now. Weak or nonexistent relationships sit at the center of problems around the negotiating table, according to experts who provided insight for this article. As noted above, some negotiations include personal attacks – an odd, dispiriting development. Without relationships, there’s no built-in trust, no ability to read the other side’s actions or words – typical buffers that prevent conversations from turning nasty. In the legal world we hear of plaintiff and defense attorneys having lunch together, meeting for drinks after court. On the surface, it feels strange to be dining with the enemy. But the outcome is often far more amicable and productive in legal proceedings. Healthcare could use the same approach. It’s time to network and meet with counterparts regularly so that the personal relationships can help soften the rough edges of negotiation.

The need for better relationships extends to employers and brokers, as well. As providers struggle to match up with payers, the employers who are effectively paying for care and whose employees make up the patient base can be strong allies. In our experience, this doesn’t happen nearly enough. Same thing for insurance brokers, who are often so key to connecting the various pieces of the how-do-we-pay-for-care puzzle.

In all of these networking conversations, providers must always take the high road. Everything should be about improving the health, access, experience and comfort for those receiving care. It’s all too easy for patients to get lost in the skirmish, but providers must intentionally make them the focal point.

Profanely

This is a no brainer. Just @%!# do it.

Providers save lives. They drive innovation. They employ millions. The provider side of the industry is not without its faults, and we should not hesitate to call out problems and bad actors. Ultimately, though, it is the providers who deliver care. Make that point in public and in private. Step up efforts to ensure every aspect of your organization is aligned with its mission. Make the case with data and stories, and don’t behave in ways that could give critics fresh ammunition.

As insurance companies increase the pressure, consolidate and integrate with providers of their own, delivering on their mission and showcasing how they’re doing it is the best way for hospitals and health systems to maintain trust take the financial steps necessary to keep the doors open.